Highlights -

Workers' compensation premiums in Oregon totaled $766.7 million for the

2009 calendar year, down 18.9 percent from 2008.

Liberty Northwest led

all private insurers in 2009 with $74.9 million in direct premium written.

Private insurers' overall

loss ratio worsened in 2009, decreasing to 66.2. SAIF's ratio increased

to 88.6. The average loss ratio for privates and SAIF decreased to 79.1.

SAIF, private, and self-insurers

experienced premium decreases in 2009. Private insurers' <more>

Introduction - Under Oregon law, each employer within the state must select one of three workers' compensation insurance options: self-insurance, insurance through a private insurance company, or insurance through the state fund (now SAIF Corporation). This report summarizes workers' compensation premiums and <more>

Figures in this report are based upon a concept of total-system written premium, which includes direct premium written from Annual Statements filed by insurance companies, earned large deductible premium credits for private insurers, and self-insured employers. <more>

Figure 1 shows annual workers' compensation

total-system premium volumes in Oregon from 1990-2009. Total-system market share information

(for SAIF, private insurers, and self insurers) is detailed in the table of data below

Figure 1, <more>

Of the top twenty companies shown

in Table 2, Liberty Northwest Insurance Corporation showed the greatest absolute decrease

in premium of $35.7 million. Three firms from the top 20 in 2008 were <more

text and figures>

Generally, loss ratios are calculated by dividing some measure of losses (or claims costs) by some measure of premium. Claims costs are comprised of indemnity payments such as time loss, temporary and <more>

There are numerous methods to quantify the profitability of Oregon's workers' compensation market. One widely used measure is the combined ratio. Although there are two different ways <more text and figures>

Dividends are largely a function of premiums and profitability from a year or more in the past. For that reason, the ratio of current year's dividends to prior year's premium is worth noting when comparing year-to-year dividend <more text and figures>

The National Council on Compensation Insurance (NCCI) is the rating bureau for workers' compensation insurance in Oregon. They have established over 500 rating classifications and are charged <more>

When Oregon's legislature created SAIF in 1965 they established a three-way workers' compensation system and provided that, if requested by either SAIF or NCCI, the Insurance Commissioner <more text and figures>

Although self-insured employers do not pay premiums for workers' compensation insurance, the Workers' Compensation Division calculates a simulated net premium for each self- insurer as the basis for the <more text and figures>

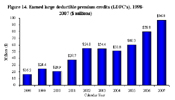

In 1996, Large Deductible Premium Credits (LDPCs) were added as an option to workers' compensation in Oregon. Under deductible policies, the insurer continues to administer all workers' compensation <more>

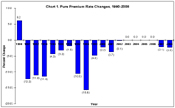

Oregon has employed a competitive rate-making system for workers' compensation insurance since July 1, 1982. Under this system, the rate-making authority (National Council on <more>

Premiums are not the only costs to employers (and employees) for workers' compensation coverage. Two other substantial costs are premium assessments and the Workers' Benefit Fund assessment. <more text and figures>

Site Map

Site Map